Happy Tuesday to you. Hope your week is off to a nice start. Here are the money topics we'll dive into today:

To ensure you are getting The Gist every Tuesday and Thursday, please move it to your primary folder (Gmail), or add it to your VIP (Apple Mail) or favorites (Outlook)!

BANKINGShould you jump on the challenger bank bandwagon?

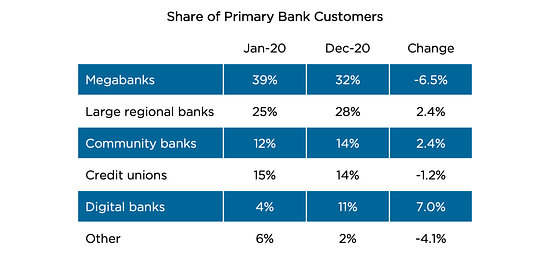

The banking industry sure is changing! There is now a slew of new banking service companies challenging the traditional banks giving them a run for their money. Aptly referred to as challenger banks, these new banking services offer a new dawn for the American consumer: low-cost or no-fee accounts, early access to wages, no overdraft fees, automated savings and more. What's more, many challenger banks aren’t actual banks but rather banking services that depend on other banks to facilitate their transactions. In fact, only a very small number of challenger banks actually have bank charters in hand—Varo, Marcus and Ally are a few that come to mind. Just don't expect their local branches to pop up any time soon! Mainstreaming of all digital banking While the world went fully digital in 2020, challenger banks like Chime, Varo, Current, SoFi, Current, and Aspiration came out big winners attracting new consumers whose needs, simply put, weren’t met by traditional banks. Meanwhile, megabanks like Wells Fargo, Chase, and BofA all lost market share of primary bank customers in 2020.

And if you're wondering how challengers make money... the vast majority of them do so via interchange fees that merchants pay to banks when customers use their debit or credit cards. And beware, some also make a hefty buck charging out-of-network ATM fees. If you haven’t yet jumped on the challenger bank bandwagon, should you? If you’re not quite sure whether you want to open an account with a challenger bank, here is what it boils down to: 🌟 Fees. If your current bank requires you to maintain a minimum deposit, or you're paying high overdraft fees and other bank charges, you should consider switching. Fees can creep and add up. In fact, the average US household pays $329 per year in bank fees alone. 🌟 Cash access. Many challenger banks allow you to get access to your wages two days early, and some others allow cash advances. Is this something you need now or think you'll need later? When pandemic lockdowns thurst millions of Americans into unemployment, quick and easy access to money became even more attractive. 🌟 Supporting a mission. Not all challenger banks support a higher cause, but some do. Aspiration, for example, offers socially-conscious and sustainable ways to spend or save money. How much does it matter to you to be mission-aligned with your bank or bank service? 🌟 Access to useful tools and features, like in-app budgeting, credit builder resources, auto-savings into customized buckets are just a few examples offered. If you use a separate paid budgeting app, you may be able to save yourself some money. One Finance and Empower are two challenger banks that come to mind offering budgeting tools within their app. Our take. The journey to modern, low-fee digital banking services has only just begun. According to Cornerstone Advisors, by the end of 2020, 15% of Gen Zers and Millennials considered a checking account from a challenger bank their primary account, up from 4% in Jan 2020. PRESENTED BY FUNDRISEThe 20% rule in investing. Only for the ultra-rich?

Investing experts will tell you that a 60% equity, 40% bond portfolio is how most investors should be allocated. Turns out this plain-vanilla strategy works fine for more of us since it's simple and manageable. But what if you tweaked your investment portfolio to add at least 20% toward alternative investments, an asset class with little or no correlation with traditional, publicly-traded assets? Why we’re talking about the 20% ruleCreated by the Chief Investment Officer of the Yale Endowment, David Swensen, the 20% rule is a diversification strategy that aims to reduce portfolio risk and in turn maximize return potential by allocating at least 20% of an investment portfolio toward alternatives. These investments fall outside the scope of traditional investments because they are usually traded in private markets, an area not well known except to the likes of the ultra-wealthy. And according to an analysis of a 19-year period by Blackstone, investors who diversified into real estate following this "20% rule" have historically outperformed those who didn't. That’s where Fundrise comes inPrivate real estate investing has traditionally been the playground for the rich, but Fundrise brings you: 🏠 accessibility—invest with as little as $500 🏠 durability—they’re all about long-term investing 🏠 technology—the platform is intuitive and easy Make 2021 the year you diversify your portfolio. Explore Fundrise. (Here are all the legal disclosures we know you'll love reading.) TAXESTax tips to help you prepare for April 15

2021 tax filing season has begun! While the IRS delayed last year's tax deadline, it's not expected this year. So, mark your calendars for April 15th and review these quick tips to help you get started on the right foot. Check to see if you qualify for free filing Did you know that you may qualify to file your taxes online for free? The IRS has a free filing lookup tool and you can also check these free filing resources directly:

Determine whether you'll be taking the standard deduction or itemizing Do this early in the process to help you determine whether you need to round up supporting documentation for itemized deductions. For many households, the biggest-ticket deductible items include state and local taxes (including property taxes), which are now capped at $10,000 per household, charitable deductions, home mortgage interest, and medical expenditures in excess of 10% of your adjusted gross income. If your itemized deductions total less than $12,400 for single or $24,800 for married couples filing jointly, you're better off with the standard deduction, which means fewer papers to get in order! Use a checklist to help you get organized Leverage a tax checklist to help you get organized and stay on track. If you're working with a tax preparer, share the checklist with them. Around this time of year, W-2s and 1099s, which report various types of income, are starting to roll in. If you don't have all of the 1099s you need, log in online to your provider's website to see if those are ready. Make IRA and HSA contributions as soon as possible Your deadline for contributing to an IRA or HSA for 2020 is on April 15, 2021. Don't wait until you get your taxes in to tackle those tasks. If you want to deduct your HSA or IRA contribution on your tax return for last year, you'll need to make that contribution before you file your return this year. Need a quick refresher? Take this quiz-based lesson to help jog some tax savings tips!

✨ TRENDING ON FINNY & BEYOND

How did you like The Gist today? (Click to vote) That’s it for today. If you’ve enjoyed today’s edition, please invite your friends to join Finny. Have a great rest of the week! The Finny Team If you liked this post from Finny: The Gist, why not share it? © 2021 FinnyNL Unsubscribe

|

Tuesday, February 16, 2021

📈 The 20% rule in investing

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment