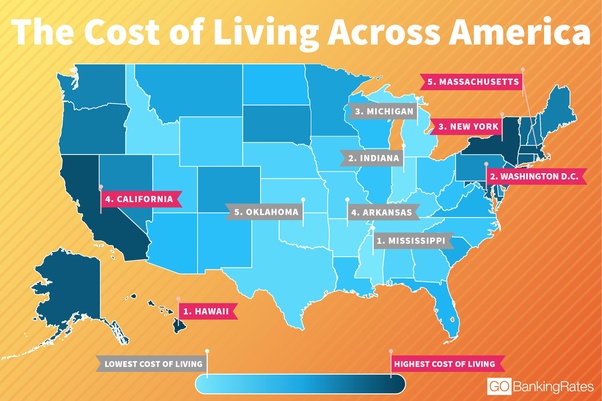

| Changing locations is becoming more and more commonplace in America. People are no longer staying local and working a union job until they get a nice pension and retire. The dynamics of employment are changing, and so are our living situations. Based on the reports we heard in 2020, you might've thought a biblical level exodus was taking place in California as reports of residents vacating the state for cheaper locations continued to spread. California actually netted about a 135,000 resident loss in 2020. So, maybe not quite as dramatic as the bunch Moses supposedly led out of Egypt. Is it really worth it though? Moving is a hassle, costs money, and let's not forget often means a career change. Is moving your life to a cheaper location really worth the difference? Comparing the cost of living in different locations The cost of living index sets a base city rating of 100. Below this would be considered cheaper than average, and above it, the opposite. Mississippi has the lowest COLI number of 2021, coming in at 86.1. Arkansas follows with an 86.9, Oklahoma at 87, and then 9 other states that sit below 90 such as Georgia, New Mexico, Wyoming—pretty much the places you'd expect. The national average in 2021 is 104.63, but let's consider the fact that we have two extreme outliers in California and Hawaii. California has a rating of 151.7, and Hawaii is at 192.9. In other words, there are a lot of places to choose from that are within the reasonable range. Home prices The median home valuation in Georgia is bout $176,000. In Illinois, it's $194,000. Arizona is $225,000, Texas is $172,000, Montana $230,000, and Vermont $227,000. Noticing a pattern? They're all within about the same $100,000 range. Out of all 50 states, 26 have a median average home price below $200,000. 15 fall between 200K and 300K, and only 9 above that. Of that 9, only 2 medians sit above $300K: California and Hawaii. They're also extreme statistical outliers, sitting at $505K and 615K each. So, what does all this mean? That there's a lot of places to live for a reasonable price, and moving just because of the cost of living is only applicable to a few groups. Questions to ask yourself If you're considering moving, it's important to objectively analyze your situation. How will moving help me meet my short or long-term goals? How much am I paying to live where I do, and what am I getting in exchange for that? Could I obtain something comparable or even better somewhere else for a lesser cost? How will this impact my career, my family, or life as a whole? Our Take. There are plenty of good reasons to move that go well beyond financials. But it's important to be honest about those reasons because most people won't find themselves in a situation where they're paying an exponential cost of living comparable to the rest of the country. |

No comments:

Post a Comment