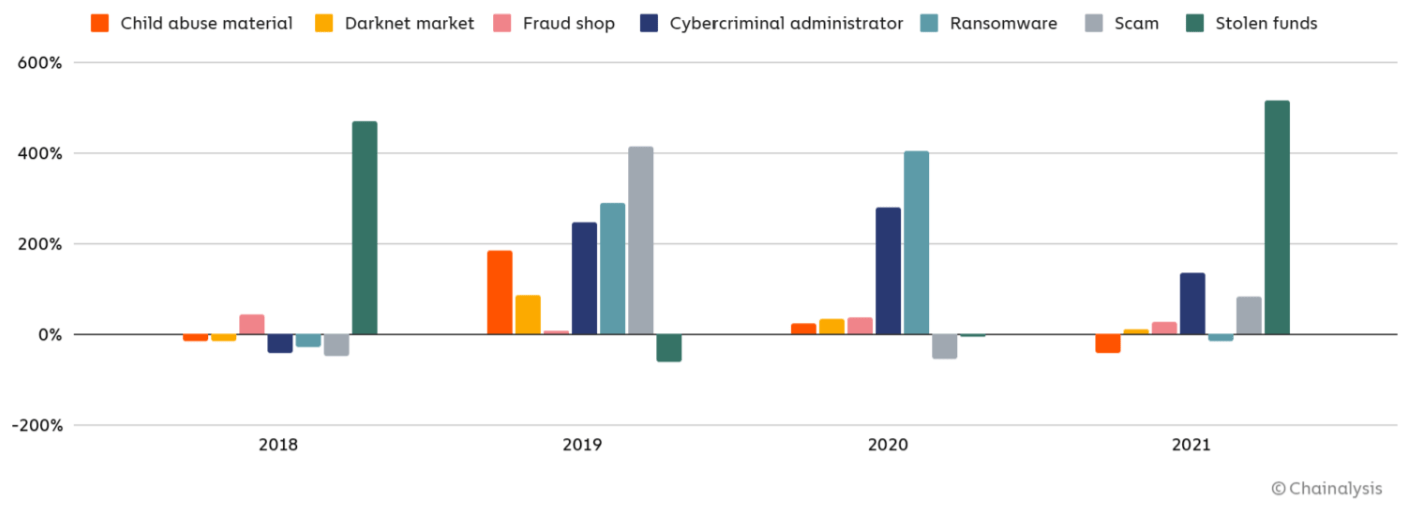

| Calling NFTs new would be an understatement, especially when we consider them against traditional investments. The first NFT was just minted back in 2015—that’s 6 years after the first crypto, 19 years after the first ETF, and about 400 years after the first stock ever was issued. An investment niche that young—with such nascent, complex technologies behind it—is bound to have its early flaws, right? Right, well… we find ourselves in that early stage right now, and it’s clear that there are still some kinks to work out. Problems with being a newbie NFT hacks are being reported multiple times per month, and you have to wonder why they're subject to so many of them. Crypto and NFTs have many new caveats and vulnerabilities that are susceptible to being exploited by highly intelligent hackers who know what they’re doing. Some of the holes are within the tech infrastructure, while others require cooperation, deceitfully obtained most often, like with phishing and airdrop scams. All of these loopholes have sent illicit activity through the roof, with the Bored Ape heist being the most recent during a very busy month of April—which will reportedly go down as the most hacked month in crypto’s history. Types of cryptocurrency-based crime in 2021 by transaction volume

Protect yourself NFTs have risen in popularity at breakneck speed over the last 16 months. Weekly trading volume shot from $27M at the end of January 2021 all the way to $1.07B by August, and remains over $150M per week still, even after cooling off. With so many newcomers jumping in, more and more traders are becoming exposed to losing money via hacks if they’re not taking at least some precautions. Not everything can be prevented, but we can do our due diligence. - Kick all the tires: There are more than enough scams and rug pulls going around in the budding crypto space, and they are probably the easiest risk to avoid. If it sounds suspect, it probably is. Do your due diligence on each project, identify the creators, read the roadmap—all the basics.

- Don’t buy stolen assets: OpenSea facilitates 95% of all NFT transactions, so they have huge leverage in regulating the NFT space. Notably, they block an NFT from changing hands when someone reports that it has been stolen. What’s problematic is that when the stolen asset changes hands before it’s blocked, and innocent buyers purchase it, they can end up holding an illiquid asset. At a minimum, before you make an NFT purchase, check the owner’s transaction history to make sure they’ve held it for a long enough time and that they aren’t flagged on OpenSea for suspicious activity.

- Delay your airdrop claim: The Bored Ape Yacht Club (BAYC) heist was probably one of the harder ones to avoid falling prey to, even for connoisseurs. Hackers broke into the official BAYC Instagram account and posted a link for holders to claim a token airdrop for their new metaverse platform. To claim an airdrop you’d have to sign a smart contract that would assess your transaction history to determine how much you were eligible to receive. But what this smart contract allowed was for the assets to be transferred out of your wallet instead. A best practice to avoid such murky waters is to delay claiming airdrops by a day or two. This way you can listen for feedback on community channels (e.g. Discord and Twitter) and look up evidence of airdrop transactions on-chain.

🖼️ Here's a related lesson on the basics: |

No comments:

Post a Comment