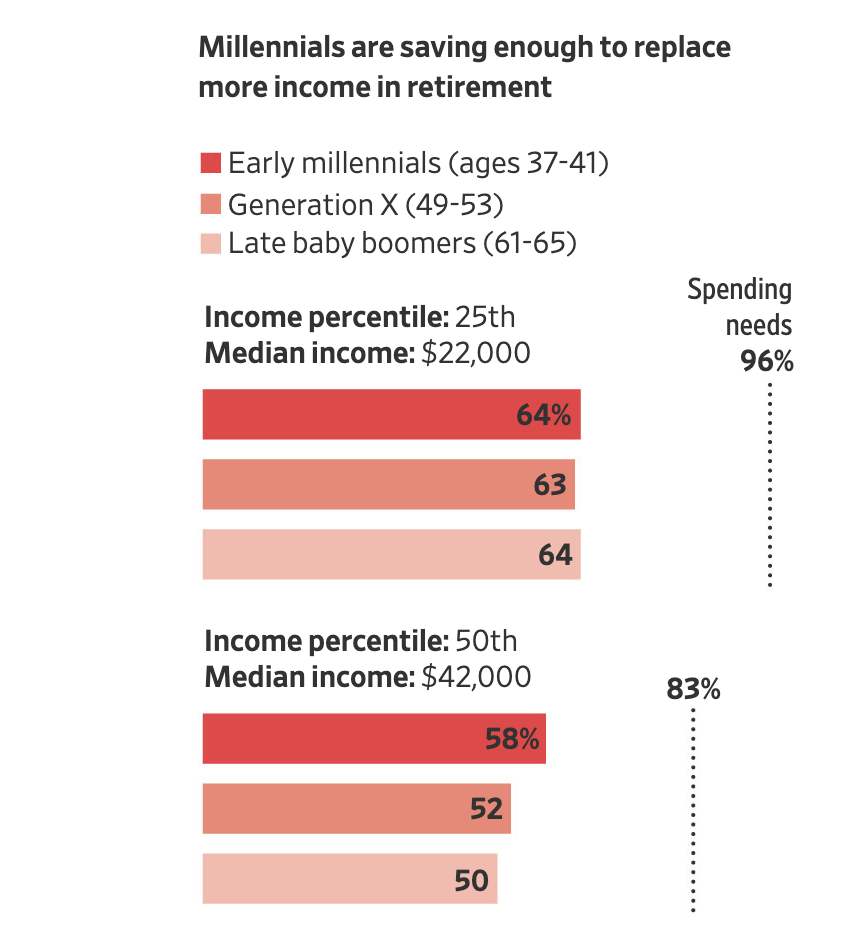

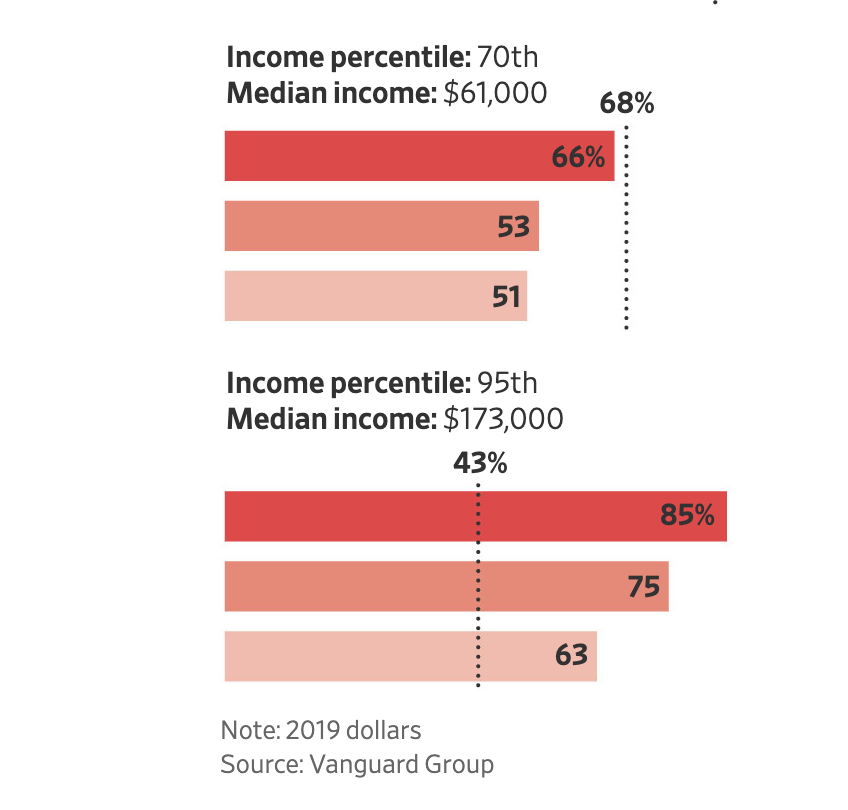

| The 401(k) as we know it today has become something unfamiliar to its origins. It was largely overlooked for two years after its inception into the Internal Revenue Code (IRC) under section 401(k) and has since become the nation's primary form of retirement saving. But the 401(k) did more than create an account — it changed the way we plan for retirement, and helped popularize other forms of retirement accounts in the process. Before the 1980s, planning for retirement income depended on a few things — hope you had a pension, Social Security, savings, and family. As a result of the trend it started decades ago, investing for retirement has now become the norm, and the pioneering generation's descendants are officially surpassing their ancestors in retirement planning. The numbers When it comes to replacing their income in retirement, millennials are set to outpace Gen Xers and Baby Boomers across all income brackets. Millennials in the 25th income percentile are tied with Boomers, on pace to replace 64% of their working income so far, and we can obviously expect this to increase as they keep working. As you climb the income ranks, the gap grows. Millennials in the 50th percentile outpace Boomers by 8% at 58% of income, lead by 15% in the 75th percentile, and have a 22% lead on Boomers in the 95th percentile of income, having saved enough to replace 85% of their income.

What's changed? - Mostly, it's the fact that investing for retirement has become the norm. It's an idea that advisors, employers, friends, family, and now social media too, have been hammering home for years now, and it has taken hold.

- There are about 1,700 employers that use Vanguard for their 401(k) services, and almost 60% of them enroll their new hires automatically — a massive leap from the 10% recorded back in 2006.

This is a good sign, but not a complete picture. Obviously, younger generations are also struggling with aspects of financial life that their ancestors didn't — like buying a home, starting a family, etc. Regardless, it's an uplifting signal that younger investors do care greatly about their prospects of financial wellness in the future, and they're acting on those desires accordingly — it's our job to continue empowering them. |

No comments:

Post a Comment