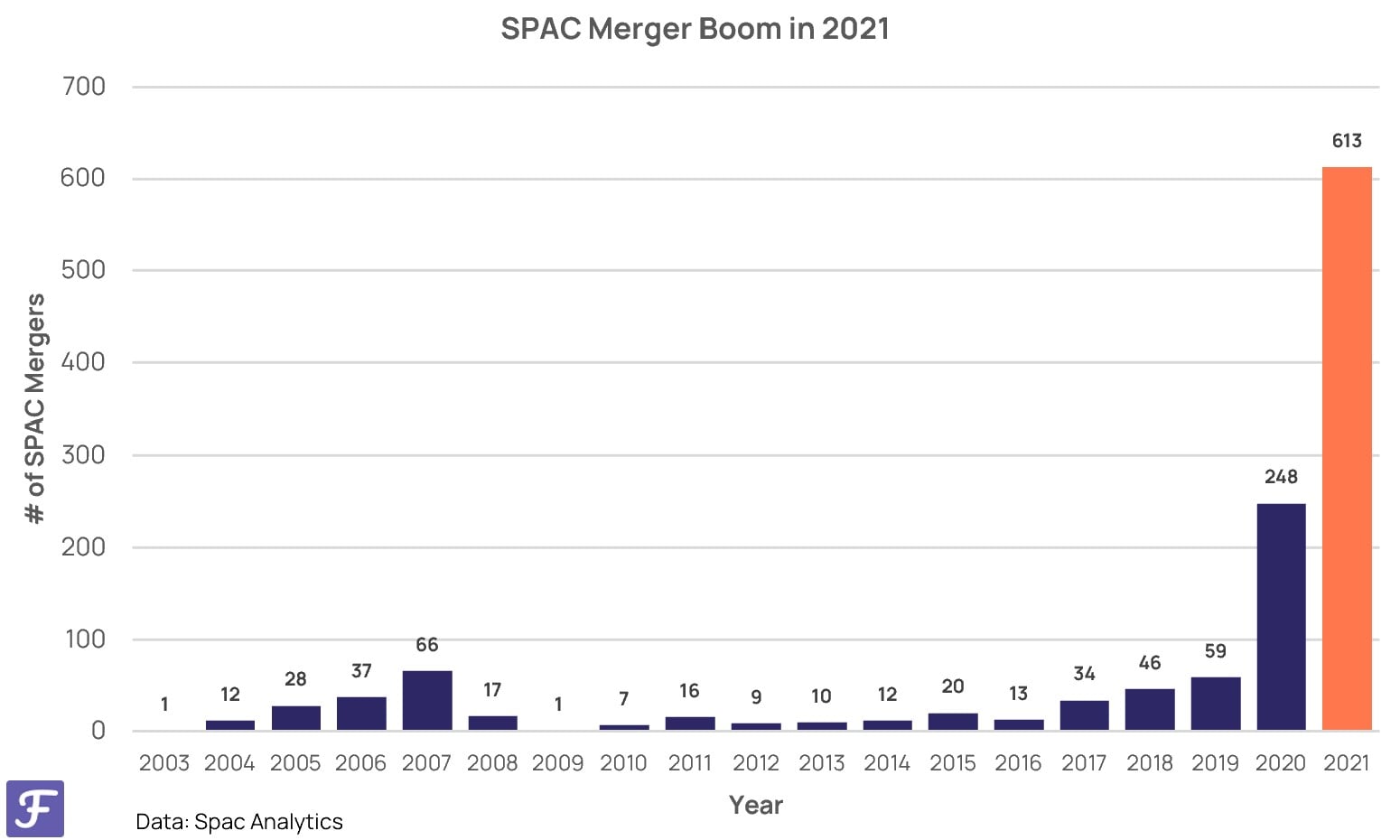

| Special purpose acquisition companies have become somewhat of a trend over the last couple of years, but they're actually not that new. The first SPAC was created back in 1993 when GKN Securities developed a template for these so-called "blank check" companies. But, they were nowhere near as popular back then as they've become today. The number of SPAC IPOs has been boosted exponentially, jumping from 59 ($13.6bn total raised) in 2019 to 613 ($161.7bn) in 2021.

Wait, what exactly is a SPAC again? SPAC is an acronym for "special purpose acquisition company." These companies are also commonly known as "blank check companies" that are publicly traded shell corporations created to acquire a private company and take it public without going through the more onerous, traditional IPO process. SPACs are formed by sponsors, typically management groups and venture capitalists, and usually proceed through two different stages. The first is to register the offering and sell redeemable securities for cash, primarily to big-ticket investors like hedge funds and other institutions. Second, they proceed to seek out, negotiate, and acquire a business in the two-year time frame following IPO. If the blank check company fails to identify a target company and complete their acquisition within two years, the SPAC is to be liquidated. The funds raised would be withdrawn from the trust and redeemed by investors at their pro-rata price, which is usually $10. Still an emerging trend This recent boom of growth in the demand for SPACs and their popularity has led to some understandable concern for the legitimacy and validity of SPACs. In fact, there are over 100 active lawsuits against sponsors as claimants seek resolution for a variety of alleged failures, including transparency, conflicts of interest and mismanagement. 2021 saw a 420% increase in securities class actions filed against SPAC-related companies from the year prior. With so many filings, many are wondering about the credibility of both the management groups involved and the soundness of the private businesses being acquired. Have SPACs grown too fast? Possibilities for the future - Cooling off: More often than not, most things tend to regress toward the mean over time. So, although SPACs have increased 10x in popularity over the last couple years, that doesn't necessarily mean this trend will continue into the future. We're already seeing rising levels of apprehension around them as investors continue to learn and adapt. In fact, after the Q1 surge of companies going public via SPACs, the figures dropped off in subsequent quarters through year-end.

- Evolving further: SPACs are just another method of going public, and yet another financial vehicle in a pool of seemingly millions. These things are constantly changing and evolving, and we see that even now with the increasing popularity of direct listings alongside them. The future of SPACs might very well be a mix of what we have now as the process of going public continues to adjust.

- Regulation: There will be greater scrutiny from regulators and ongoing litigation from investors. As the SEC is already ramping up its enforcement actions, sponsors are being advised by their lawyers to more thoroughly vet a potential target's business and to increase transparency around conflicts of interest and other issues that could spark lawsuits. That may be why we're seeing a growing number of SPAC deals falling through before the listed shell merges with its acquisition target.

- Rebranding: And because SPACs are still in their early days, it makes sense we'll see a few bad apples that will bring some needed adjustments. While they may be painted as risky, "easy money" assets by nay-sayers, it's entirely possible that SPACs will become more refined over time, and undergo a deserved rebranding as a result.

For now though, the SPAC market will likely continue to provide an attractive avenue to bring private companies public, although getting deals done may be getting harder for sponsors. But remember, not all SPACs are created equal, and if you are considering buying, we'll state the obvious: understand your risk tolerance and do your homework. 💡Need a refresher on fundamental analysis? If so, take this microlesson on the topic: |

No comments:

Post a Comment