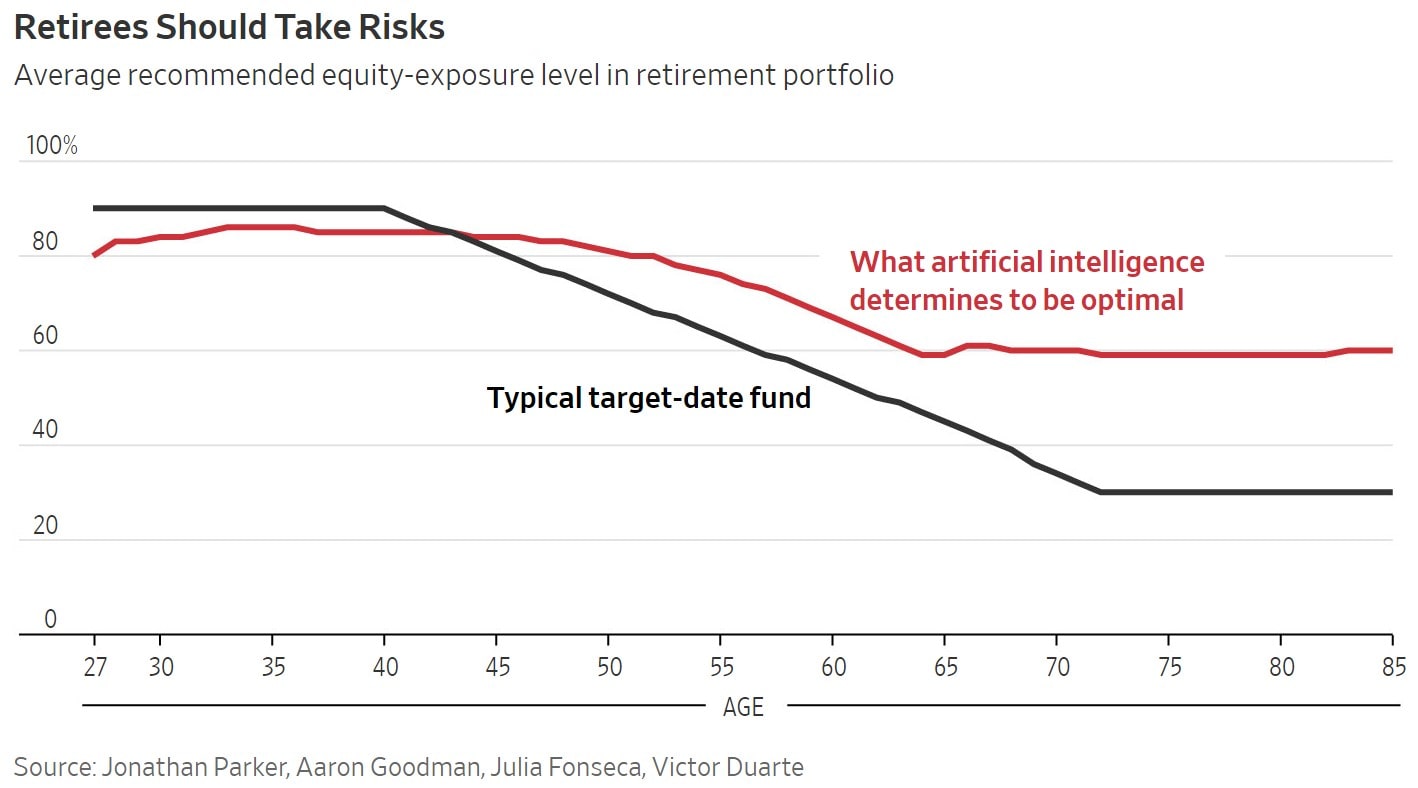

| Wells Fargo and Barclays Global Investors introduced the first target-date fund back in 1994, making them a spry 28 years old, and relatively young in the financial world. They were designed mostly with the “do it for me” type retirement investor in mind, aiming to meet the needs of busy professionals without much time to invest on their own. This of course came at a time when self-directed investing was nowhere near as popular as it is today and far from accessible as it is now either. While target-date funds do maintain their appeal, we’re also beginning to learn more about their shortcomings that date back to their origins. The path of a target-date fund Target date funds are tailored to an investor's anticipated retirement year, and so they're also tethered to your age. They start out with a higher allocation toward equities, usually about 90% prior to age 40. After this, they meander down toward 50% as you near retirement age, ultimately dropping as low as 20-30% equity if the fund is held through retirement. That sounds pretty logical on the surface—a fund that’s designed to optimize its allocations based on my age? Perfect, right? Yes, they’re certainly better than nothing, and perhaps even perfect for someone who really wants a hands-off approach to managing their nest egg, but this so-called “glide path” has some inherent biases, and it seems to be falling short based on some new data. How target-date funds might fall short Recent research from the National Bureau of Economic Research suggests these funds might be overly conservative, which is something that could cost passive investors a lot of money, maybe even a comma or two. Researchers turned to a budding branch of artificial intelligence (AI), often referred to as deep learning, to mint this data. Simply put, the AI was put through what they dubbed “the game of life” to account for the “risky economic environment in which people earn, save and invest over their lives.” Its goal was to solve the optimal allocation to equities over time. The outcome? After running this simulation countless times, the result was an AI-crafted glide path that never falls below a 60% equity allocation at any point along the lifetime of the account holder.

Source: WSJ Viewing retirement investing through a personal lens A commonly followed proverb of investing is to trust facts over feelings. This is seen in everything from buying the dip, holding through crashes and dollar-cost averaging. The takeaway is to ignore the micro for the sake of the macro. Although these funds undoubtedly use data to generate glide paths, it seems that the algorithms behind existing target-date funds might be a bit emotional, potentially leading investors astray as it tapers out of equities with age. What’s the solution, then? Make your retirement investing more personal. Account for your own age, health, dependents, financial situation, career, risks and retirement goals, and only then decide how to invest, adjusting as things change. You might still come to the conclusion that a target-date fund is perfect for you, and that’s certainly a fine outcome. The larger point here is perhaps that it may also be worth doing some healthy second-guessing before investing. |

No comments:

Post a Comment