TOGETHER WITH  | Good day. Can you guess who is the second-largest shareholder of Tesla, behind Musk himself? a. Vanguard, b. Warren Buffett, c. BlackRock. Follow the wave 🌊 below for the answer. Here are today's money topics: - A U.S. housing market update

- What is a lazy portfolio?

- How the updated 529 rule makes saving easier

| |

HOUSING Another U.S. Housing Market Update | | | | Most of the time, the housing market is a pretty boring machine — chugging along in a slow and steady fashion, reliably increasing its value in aggregate and over the long haul. In recent years, that's been anything but the case. Just like everything else, home prices have become higher and more volatile over the last 24 months. So, as a result, here we are again with another housing market update. And yes, this one is just as perplexing as the rest. Behind the latest - Small leap: Data from last month shows that sales of previously owned homes jumped by 14.5% from January to February, marking the first month-over-month gain in over a year now, and the largest jump since July 2020.

- Perspective matters: Despite that spike, the bigger picture tells a different story. In the wake of rising interest rates and lofty prices, home sales have declined -22.6% compared with February of 2022.

- Prices, however: Although month-over-month sales rebounded, prices remain stuck in limbo. Median home sale prices in the U.S. fell by -1.2% in the month of February relative to the last year, which is the first year-over-year drop we've seen since 2012.

- Rates remain high: Since their spike to nearly 7% in late Q4 2022, the average rate on a 30-year fixed-rate mortgage has come down to roughly 6.42% thus far this year. That calm down may be enticing to some prospective buyers, but the reality is that rates are still the highest they've been since roughly 2002, representing a valiant headwind for the housing market.

- Projections for 2023: Zillow and other similar outlets expect home prices to remain under pressure in 2023 before returning to a more normal growth rate next year. As for rates, the Fed is expected to end the year with a funds fund rate of roughly 5.5%, and Realtor.com anticipates the 30-year fixed to finish 2023 at about 6.2%.

Take this related lesson and earn 🟡 Dibs: | | | |

INVESTING What Is A Lazy Portfolio & Does It Actually Work? | | | | Investing over the long term has proven to be a wealth builder, and far less risky than not investing at all. The reality for most though is that if you did nothing but invest in a few simple index funds and forgot about it, you'd be doing great a few decades later. And there's actually a strategy for this and it's called the 3-fund portfolio. In theory, investors just hold a total U.S. stock market fund, an international stock market fund, and a total bond market fund, and be done with it. So how does it work? A few things to note - Customization is a-okay. The 3-fund portfolio is just one example of lazy investing that can work for you. You can create your own portfolio with an index fund and an asset makeup of whatever you please and still have your viable lazy portfolio that can work for you.

- Allocation will play a big role in your returns. Whether you decide that one total market fund or three funds suit you best, how you allocate your funds across those 1 or 3 makes a big difference in your returns. Make your allocations based on your risk tolerance, time horizon, and future financial goals you want to achieve. If you don't know where to start here, learn more about the rule of 110.

- You don't have to abandon other investments. If you enjoy scouting out businesses' balance sheets like they're some sports draft highlight reels, then, by all means, keep doing that. Be aware of the risks you're taking with any concentrated bets, and consider adding a complementary lazy portfolio strategy if you aren't already.

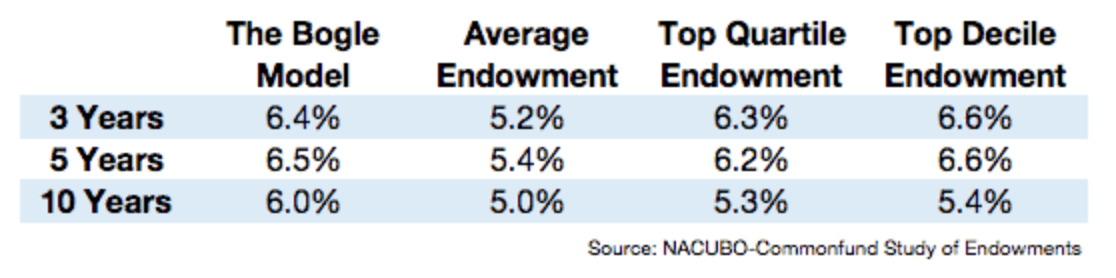

- And last but not least, the results of a three-fund portfolio have continued to shine compared to professionally managed endowment portfolios. Below we show the results of a lazy, 3-fund portfolio of Vanguard ETFs ("The Bogle Model" attributed to the Founder of Vanguard, Jack Bogle) compared to 800 college endowments. Over a 10-year period, The Bogle Method outperforms even the top-performing endowments.

Take this related lesson and earn 🟡 Dibs: | | | |

FEATURING MONARCH | | | | Monarch simplifies money management for couples with easy budgeting, goals, net worth tracking and more. See all your finances in one place, categorize expenses automatically, and collaborate with your partner to achieve financial goals. Try Monarch now, with a free 7-day trial and cancel anytime. | | | |

FINANCIAL PLANNING The Updated 529 Rule Makes Saving Easier | | | | 529 plans are like an extremely specialized tool. They're great at what they do, but often viewed as narrowly focused and not allowing much flexibility when it comes to their uses. While these accounts are great for educational savings, their limitations often have costly consequences in the event of an emergency or deviations from the plan. Luckily though, recent updates made by the Secure Act 2.0 are making the 529 even better. What's the update? - 529 basics: 529 plans are educational savings accounts that can also hold investments, and allows for parents and/or relatives to save for a child's future educational expenses. They're kind of like a Roth IRA for college — meaning your savings and investments can grow tax-free as long as they're used for qualified educational expenses.

- The penalty: Previously (and currently), any withdrawal used for unqualified educational expenses would be subject to a 10% penalty in addition to income taxes, with the only way to avoid those costs being to transfer the account to another beneficiary.

- The update: Thanks to amendments made by the Secure Act 2.0, 529 plan account beneficiaries will now have the option to roll unused 529 plan funds into a Roth IRA without incurring any additional penalties or taxes — starting in 2024.

- Strings attached: In order to qualify for this option, you'll have to meet some criteria though. For example, the 529 must have been open for at least 15 years, the Roth IRA owner must be the beneficiary of the 529, the lifetime rollover limit is $35K, rollovers count towards your annual Roth IRA contribution limit of $6,500, and 529 contributions or earnings accrued within the last 5 years are not eligible for the rollover.

Take this related lesson and earn 🟡 Dibs: | | | |

🌊 BY THE WAY | - 🔋 Answer: Vanguard is the second-largest shareholder of Tesla, behind Musk himself, with a 6.85% stake in the company; Blackrock and State Street own 3.6% and 3.13% of Tesla's stock, respectively. Tesla joined the S&P 500 in 2020, and it has since become a part of many index funds which have had to purchase the company's shares at the company's weighting in benchmarks. At the time of Tesla's inclusion into the S&P 500 index, nearly $2 trillion in index funds that followed the firm's holdings were forced to purchase the automaker's shares (CleanTechnica)

- 🌇 A tale of two housing markets: prices fall in the West while the East booms (Fox Business)

- 🍼 ICYMI. The cost of raising kids (Finny)

- 🧳 4 states that will help pay off your student loans for moving there (YF)

- 🌁 Seattle's new law gives gig workers paid sick time off (The Verge)

- 💡 Finny lesson of the day. Speaking of the S&P 500 Index, if you're not familiar with what this index is, let's review it:

| | | |

| |

| Finny is a financial wellness platform. The Gist is Finny's twice-a-week (Tues & Thurs) newsletter covering personal finance, market trends and investing insights. Finny does not offer investment and stock advice. Please support our corporate sponsor — Monarch — as they make rewards on our platform possible! If your company is interested in sponsoring The Gist, please reach out to us. And if you have any feedback about this edition or anything else, please email us. | | | | | | | |

No comments:

Post a Comment