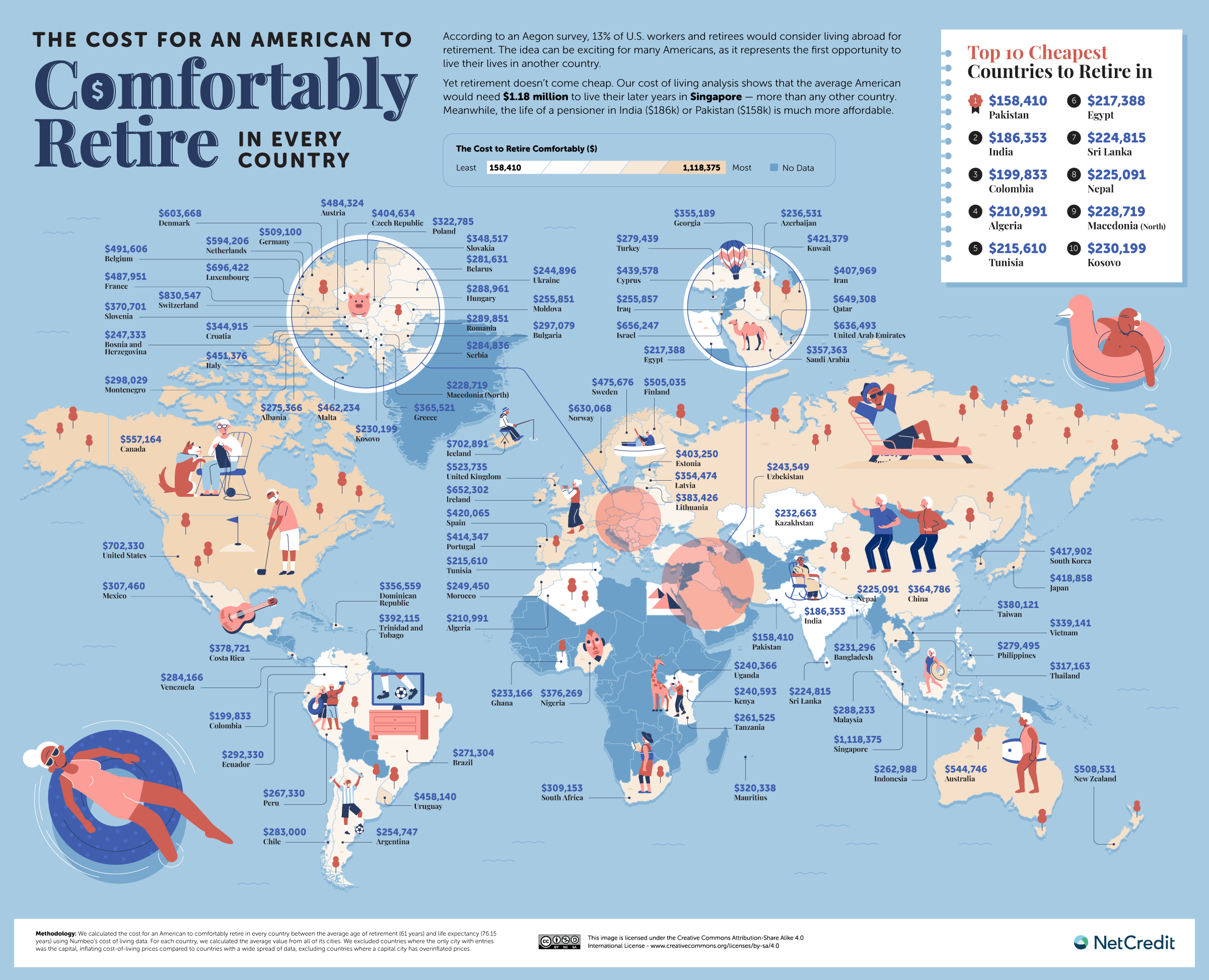

TOGETHER WITH  | Good day. According to a recent survey by Aegon, can you guess what precent of U.S. workers and retirees would consider living abroad in retirement? a. 13%, b. 23%, c. 33%. Follow the wave 🌊 below for the answer. Today's personal finance topics are: - Dividend investing — what is it & is it worth it?

- A warning from Walmart

- How to set financial goals

| |

INVESTING Dividend Investing — Is It Worth It? | | | | Dividend investing is like that "good job" your parents always wanted you to get. Sure it's safe, has decent benefits, and it pays alright, but at what cost? How long do you have to work there to reap the benefits, and is it even worth it if you hate it? Dividend investing is similar in the sense that, yes, it can provide some nice, passive income, but it also presents itself with its own intrinsic pitfalls. The basics - Companies pay out dividends to share their profits with shareholders. It's a way for them to thank their shareholders for their ongoing support and to incentivize them to continue to hold the stocks.

- Dividends are paid out to its shareholders at predetermined time intervals. This usually comes at the frequency of four times per year, quarterly, or in some cases semi-annually or annually. This can be in the form of cash, or it could come by way of more shares in the company too.

- Companies pay a set dollar amount per share basis. If you own one share of AT&T, they will pay you $0.2775 per quarter, per share owned. This makes their dividend yield about 5.9%, which is high. Yield is calculated by dividing the annualized dividend payout by the current share price.

- Dividends, especially good ones, usually come from companies that have reached maturity and find themselves in established industries with predictable profits. Think oil & gas, banking, healthcare, utilities, etc. They're beyond the growth phase where they can reinvest heavily and take on expansion debt, and they reward investors for their investment.

- What's a good dividend? In general terms, anything over 2% is considered to be a good dividend payout rate, but that's also the broad average of the S&P 500, and as seen with AT&T, you can find high yields if you're a diehard dividend fan. IBM has a 5.1% yield, Realty Income, a REIT, offers 4.7%, and Walgreens is at 5.3%.

Considerations when dividend investing - It's not a strategy to produce investment income fast, or at all, unless you have a lot of cash, a lot of patience, or both. You would need to own 1,000 shares of that high-yield AT&T stock to produce $2,000 a year in dividend income. That's a $29,000 investment, so it would take you 15 years to make your money back at present value.

- It's not for the faint of heart, the light of accounts, or the impatient. Despite this though, that doesn't mean that over time you couldn't build up a nice supplementary income. If you were able to spread a few hundred thousand dollars of retirement funds across multiple well-paying dividend stocks, this could become a viable passive-income option.

- But stock price is still relevant. Picking a dividend stock that's presently overvalued or doesn't forecast well for the long-term future can be a risky play. Sure you may be getting a great dividend payout, but if your principal investment value is melting faster than the ice caps because the market is becoming speculative of the business or the industry it's in, then you should re-evaluate your investing strategy.

It's important to pick well-established businesses with a long-term outlook — and one you also have strong personal conviction in. A dividend stock should not only create income but also preserve the value of or even potentially grow your principal investment amount. So is it worth it? Whether or not dividend investing is worth it depends on your financial goals, risk tolerance, and more. Got a lot of cash on the sidelines and want some truly passive income? This may be for you. Need some money quickly? Steer clear as there are other investment strategies for you. Take this related lesson on this topic and earn Dibs 🟡 while you're at it: | | | |

ECONOMY A Warning From Walmart | | | | If there's one thing we've learned from the last few years of economic chaos, it's that there's almost always more than what meets the eye. From inflation readings to earnings reports, we know all too well by now that these numbers can be misleading. This couldn't be more true than right now, and a recent earnings report from Walmart is a perfect example. Below the surface of the economy - Earnings misnomers: The earnings reports of retail giants are often seen as a window into the soul of the economy, and this round is no different. Walmart recently beat expectations on theirs, reporting sales growth of 8.3% year-over-year, a seemingly welcoming sign for optimists.

- But not so fast. A closer look at that earnings report would reveal that much of that growth was due to more expensive groceries, consumers shifting down from more expensive stores, and buyers moving their money away from discretionary purchases like toys, homeware, and clothing, all of which underperformed.

- Illusion of strength: Earnings like this that seem positive on the surface are akin to the most recent spending report too. Retail spending was up buoyantly in January, climbing 3% compared to its December decline of -1.1%. Unfortunately though, this doesn't tell the whole story. Sure, the consumer is spending, but it's largely because they have to.

- Consumer finances: Per a recent survey from BankRate, 39% of consumers say that their emergency savings are lower than this time last year, and 10% said they have zero cash set aside. Meanwhile, household debts also increased by 2.4% to $16.9T in Q4, with credit card debt adding $60B on its own. Suffice it to say, consumer finances aren't aligned with the illusion of strength we're seeing.

A cautious outlook Since Walmart's earnings release, large retailers across the board (Macy's, Lowe's, Target, Best Buy, Big Lots, and Lumbar Liquidators) have all reported cautious results about the consumer. And for the foreseeable future, as long as inflation and economic uncertainty are a thing, people will continue to spend more on necessities and less on discretionary items. Take this related lesson on this topic and earn Dibs 🟡 while you're at it: | | | |

SPONSORED BY VERB Great Energy, Every Day | | | | Say goodbye to overpriced lattes and hello to Verb. Verb is the perfect energy boost: a plant-based snack with as much caffeine as an espresso. Conveniently pocket-sized for on-the-go, it's made with Organic Green Tea and natural ingredients like quinoa and brown rice crisp. And it's got over 3000 5-star reviews. Try Verb. Get 5 bars free with code SAMPLER. | | | |

MONEY TIP How to Set Financial Goals | | | | Money might not buy happiness, but it sure can buy things that contribute toward it. Whether we'd like to admit it or not, money is a big key to some very important factors when it comes to quality of life — things like security, peace of mind, health, access to necessities, and simply the ability to live without worrying about the costs of all your tomorrows. And yet, very rarely does the money needed for those things come without first having a plan. Setting goals might seem like an optional extra, but the fact is that they're the foundation of achieving the life you want. Pointers on how to set financial goals - Take care of the basics: Almost no goal is achievable without having a solid foundation to start with. This is why it's so important to first begin to take care of things like budgeting and building up savings for unexpected emergencies. One of the biggest traps with budgeting is not making it realistic enough or making it so restrictive you set yourself up to fail. And leverage tech to help you budget (i.e., YNAB, Mint, etc), and if that's not your cup of tea, using tools like excel or your handy dandy pen and paper can be just as good.

- The motivation: Financial goals are hard to achieve without the proper motivations behind them. As you think about your goals, connect each of them to a deeper motivation. And who each of those goals will benefit. For example, writing a will or setting up a trust may be linked to a deeper motivation to provide security for your family.

- Prioritize: You can only undertake so many ambitions at once, and trying to juggle too many can often result in accomplishing nothing. Once you've considered your goals and motivations, to make better sense of their priorities, consider timeframes (short vs. long term) and their importance (i. essential vs. nice to have). This way, you can get a bit more organized without feeling overwhelmed.

- Layout your options: Taking inventory of what you have and consider what you need for each of your goals. This is where budgeting and documenting your income sources and expenses can help. For example, having a clear picture of how much money you can allocate to different goals each month gives you clear direction on how to move forward. Don't let analysis paralysis get the best of you though because the reality is that things change as we live our lives and inevitably, our goals will too.

- Set micro goals to boost motivation: Breaking down your ultimate end goal into smaller, more immediately achievable ones can help keep the momentum going strong. While the big picture remains at the forefront, those little micro goals will be the steps that take you there.

- Revisit: Just 'cuz you set a plan for now doesn't mean you should forget them. When goals get put on autopilot, we can often lose sight of how life might've shifted course over time. No matter how solid you think your plan is, revisit them regularly to ensure goals, actions and motivations are still in alignment.

| | | |

🌊 BY THE WAY | - 🌏 Answer: 13% of U.S. workers and retirees would consider retirement abroad. The top 3 most affordable countries for U.S. retirees are Pakistan, India and Colombia (digg)

- 🏙️ Apartment rents fall nationwide: Where are they going down the most? (USA Today)

- 🔎 ICYMI. Is dividend investing back? (Finny)

- ✈️ U.S. names and shames airlines over family seating (BBC)

- 💳 Credit card debt soars as perks proliferate (Axios)

- ✨ Finny lesson of the day. The idea of moving abroad in retirement isn't really possible without first understanding what it means to be financially independent. Amirite?

| | | |

| |

| Finny is a financial wellness platform. The Gist is Finny's twice-a-week (Tues & Thurs) newsletter covering personal finance, market trends and investing insights. The content team: Austin Payne, Carla Olson. Finny does not offer investment and stock advice. Please support our corporate sponsor — Verb — as they make rewards on our platform possible! If your company is interested in sponsoring The Gist, please reach out to us. And if you have any feedback about this edition or anything else, please email us. | | | | | | | |

No comments:

Post a Comment