Good day. The first bank-issued credit card was minted by Bank of America back in 1958, and credit cards have become increasingly popular since then. Can you guess how many the average American carries? a. 1, b. 4, c. 7. Follow the wave 🌊 below for the answer. Today's money topics are: - A Few Big Winners Are Fueling The Market's Gains

- How AI Could Take Over Personal Finance

- Think Twice Before Closing an Old Credit Card

| |

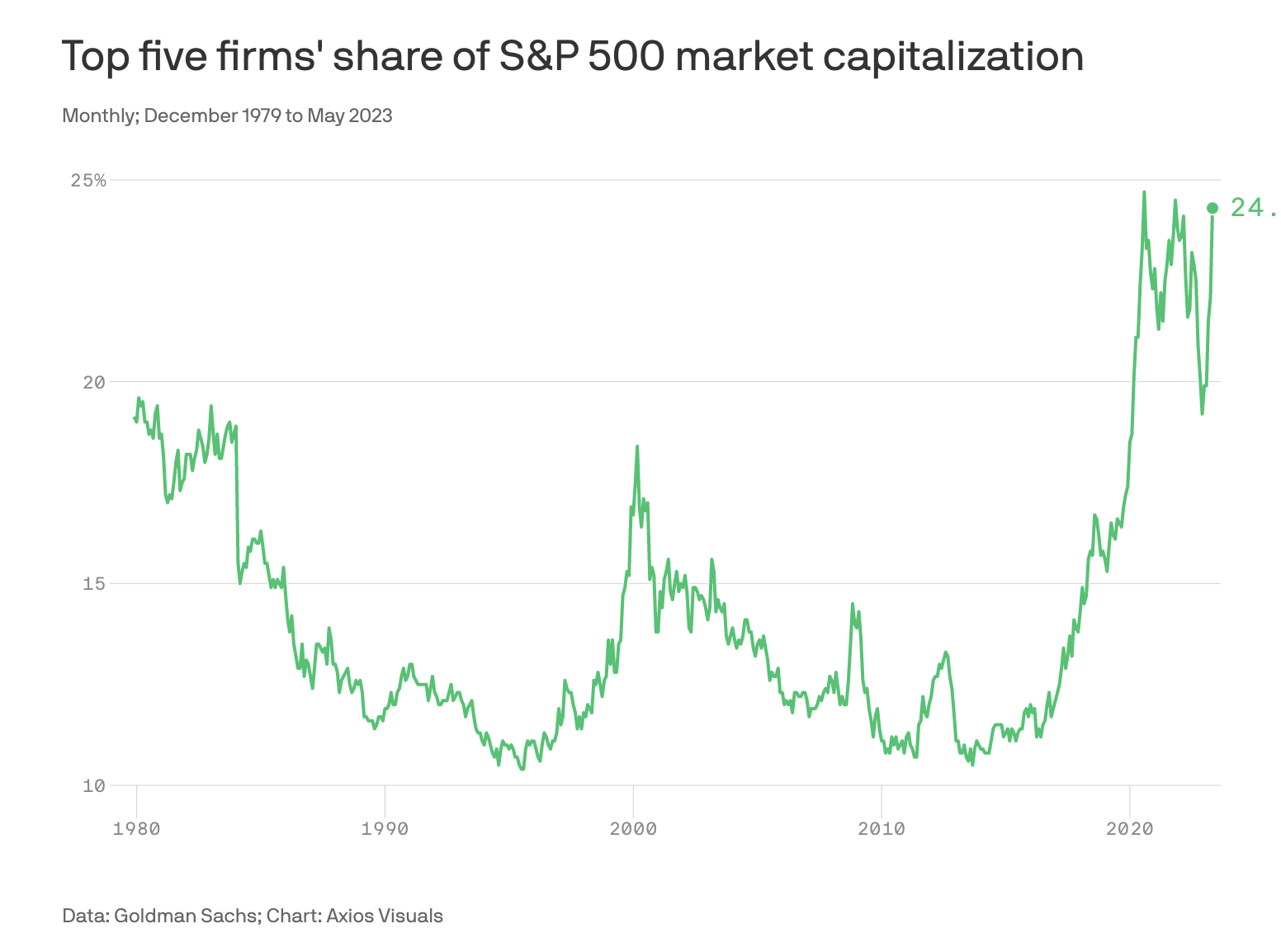

INVESTING A Few Big Winners Are Fueling The Market's Gains | | | | The tech sector has become the stock market's all-star player in recent years, and without it, there's no doubt the market's gains would be pared down significantly. Tech has taken on a heavy workload, and it's handling it with ease. Slicing up the gains pie - The year so far: After a historically rough 2022, tech-heavy indexes have rebounded nicely this year. The S&P 500 Index is up over 11% while the Nasdaq 100 Index boasts a 33% return — both triumphing over a litany of apprehensions investors have harbored all year.

- Weighting 101: In market cap-weighted indexes like the two mentioned indexes, the companies with the largest valuations have the biggest sway in the index's overall return. For example, the S&P 500 derives 27% of its weight from just 7 large tech companies, while the Nasdaq 100 allots over 54% of its weight to those same 7 companies.

- The fuel behind this year's gains lies in the tanks of some well-known tech giants like Apple (up 36% this year), Microsoft (37%), Alphabet (39%), Amazon (44%), and rising powerhouse Nvidia, which has grown by 159% in the midst of AI excitement.

- Without these 5 big names to move the boat, the overall market would find itself up just 1.5% for the year. If you were to trim further and remove Meta (up 120%) and Tesla (up 66%), then the S&P 500 would be slightly underwater.

- That's cool, but this concentration might be showing us some subtle signs of weakness. With this year's gains so dependent on these 5-7 companies, it begs the question — what's the health of the whole market and what happens when the leaders get tired?

Take this related lesson and earn 🟡 Dibs: | | | |

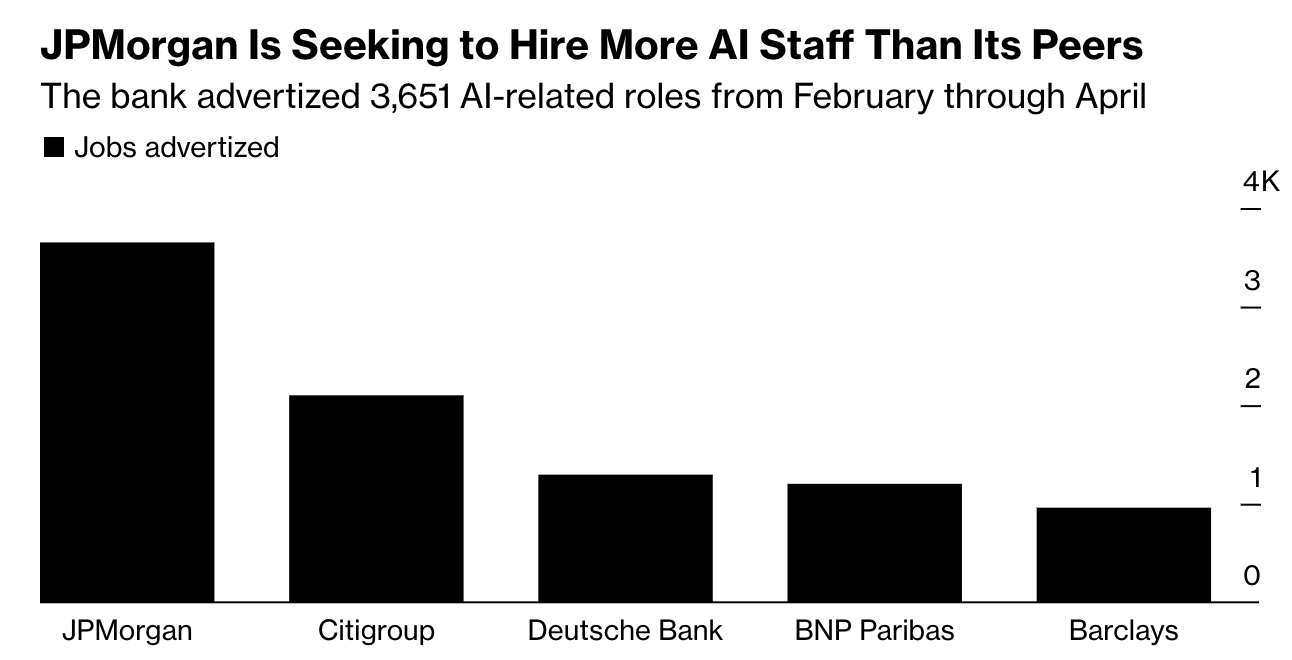

FINANCIAL PLANNING How AI Could Take Over Personal Finance | | | | Artificial Intelligence has been around for decades now, loitering in the backdrop of technology and science fiction without ever truly coming to reality. Now though, it's here. Over the last 6 months, AI and its many manifestations have taken center stage, causing both hopefulness and apprehension in the process. And nothing is really off limits for AI, not even our personal finances. With robo-advisors and self-management of our finances becoming increasingly popular, there's a sizable market here for AI to slot into. Behind the scenes - Job openings: While many fear that AI may start taking jobs, right now the truth is it's taking over job openings as financial firms increase their AI-related hiring. There were almost 800,000 AI-related job postings in the U.S. last year, and banks are catching on. Leaders like JPMorgan have reportedly seen 40% of their job postings turn AI-oriented in some fashion, while others like Citigroup, Deutsche Bank, Barclays, and others followed suit in Q1.

- Local developments: JPMorgan struck the news recently with its patent filing for IndexGPT, a financial advice equivalent of ChatGPT. Deutsche Bank is employing deep learning to analyze clients' portfolio concentration, Morgan Stanley is in the "testing stage," Goldman Sachs is using it to help write code, and countless more institutions are no doubt well on their way.

- Practical implications: From the consumer standpoint, AI began interweaving itself into our finances a long time ago, and the most recent advancements just represent a fully fleshed-out version of it. For us, AI will likely be used to analyze all of our data and provide recommendations based on that, not to mention automate a lot of mundane tasks like balance inquiries, transfers, loan apps, and more. And the final frontier? Providing hyper-personalized advice via chat platforms like those we're seeing now.

- Good, bad, or neither? There's the potential for both good and bad here. On one hand, bringing AI to finance creates a lot of benefits in the areas of efficiency, customer service, accuracy, and access to financial advice. On the flip side, you've still got concerns regarding how impersonal it might be and oh, the data security issues.

| | | |

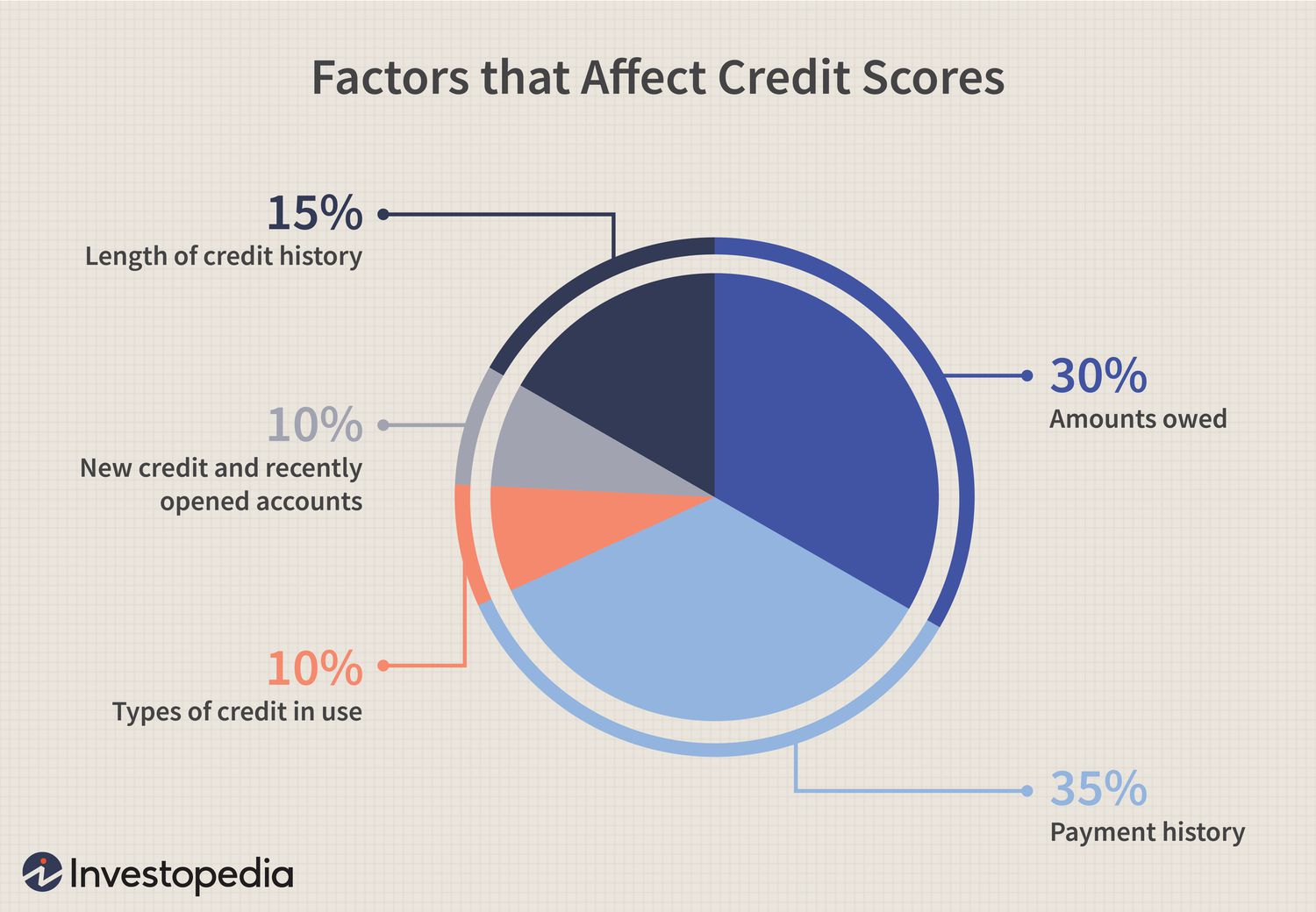

MONEY MINDSET Think Twice Before Closing an Old Credit Card | | | | Credit cards have become an increasingly common way of spending money. In fact, a 2023 survey shows that roughly 36% of all transactions are now handled by a physical or virtual credit card. That may seem bad on the surface, but the truth is that many of us use these cards as a middle-man with many benefits, not as a way to buy things we can't afford. And those credit card savants are often financial aristocrats as well, staying on top of things and keeping their finances clean and organized. Those tendencies may occasionally give rise to the desire to close out old, unused accounts, especially credit cards. But, not so fast — it might be best to keep that placeholder there. Here's why - Your score makeup: For most scoring models, your FICO credit score is made up of roughly 5 different components. The largest is often payment history, accounting for about 35% of your score. Following payment history is your utilization (30%), length of credit history (15%), new credit (10%), and types of credit (10%).

- Old account positives: Keeping an old account open does two things for your score. First, it increases your average age of account – closing a 10-year-old card, for example, could significantly drop your average age of account. Second, an extra card also increases your total available credit line, which therefore decreases your credit utilization.

- Considering it all: Whether or not it makes sense to close an old card depends on your situation. If the credit limit drop won't impact your overall limit by much or the card isn't one of your oldest and you already have a tenured history, it might be okay to close it. Additionally, if you're paying a hefty, non-negotiable annual fee for a card you don't use, this would be another valid reason to close it.

Take this related lesson and earn 🟡 Dibs: | | | |

🌊 BY THE WAY | - 💳 Answer: 4. Per Experian's most recent figures, the average American touts almost 4 credit cards with an average aggregate limit of $30,365 (Fortune)

- 🎓 Are you financially wiser than a college student? (MarketWatch)

- ⚖️ ICYMI. Debit or credit? (Finny)

- 🍔 AI comes to the drive-thru. Would you like human interaction with that? (WSJ)

- 📊 Finny lesson of the day. Credit is a double-edged sword, one that can be more harmful than helpful if it isn't used with care. Because of this, it's paramount that we understand how these tools affect our finances:

| | | |

| |

| Advisory services are offered through Origin Financial, a Registered Investment Adviser registered with the U.S. Securities and Exchange Commission. The status of registration as an Investment Adviser does not imply a certain level of skill or training. The information contained herein should in no way be construed or interpreted as a solicitation to sell or offer to sell advisory services. All content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor, is it intended to be a projection of current or future performance or indication of future results. | | | | | | | |

No comments:

Post a Comment