TOGETHER WITH  | Good day to you. Inflation figures fell again and by 0.1% in December, a number in line with expectations from economists. The biggest reason for the decrease came from a sharp drop in gasoline prices. Today's trivia: Can you guess, which of the following is a top 2023 prediction, according to Visual Capitalist? a. work culture will become more rigid, b. interest rates will peak in 2023, c. equities will see negative returns. Follow the wave 🌊 below for the answer. Our money topics for today: - Is the "American Dream" on Hold?

- Bond Buyers May Get Some Relief in 2023

- Tips to Protect Your Money in 2023

| |

PERSPECTIVE Is the "American Dream" on Hold? | | | | The phrase "American Dream" was first used by James Adams in his 1931 best-seller titled "Epic of America," calling it "that dream of a land in which life should be better and richer and fuller for everyone, with opportunity for each according to ability or achievement." The saying has long since taken on a life of its own. It's normally used to refer to a collective of ideals including home ownership, family, business success, and promoting a general sense of patriotic prosperity. But the years have not been kind to that American Dream. It's become an increasingly expensive and elusive standard of living, and the idea that it's obtainable by anyone who works hard enough is being challenged as we speak. How much does a dream cost? - Home life: Homeownership lies at the center of the American Dream for most, and it's more unaffordable than ever now. Folks in the US buying a home at the median sale price in Q4 2019 would've been paying a total of about $1,663 monthly(including home loan, insurance, and taxes), and $173,000 of interest over the life of the loan. Those same numbers would now be about $2,786 per month and $444,000 of interest. That's a 67% jump in monthly costs that now consume 47% of the median household's monthly income. If you're single or can't put down 20%, affordability becomes much worse.

- Family life: It's hard enough to provide for yourself, but providing for a family is even tougher. Thanks to inflation, the cost of everything has increased noticeably over the last year, adding insult to injury. The cost of food is up 10.6% in the last 12 months, energy is up 13.1% in aggregate, transportation services are up 14.2%, and the cost of rent has increased dramatically too.

- Education: Housing and essentials form the basis of a healthy life, but if we look at the macro, we also have a larger scale problem blooming with education costs. Over the last two decades alone, the average cost of tuition at public four-year universities has increased by about 124%, outpacing inflation by 172%. Tuition has an annual average inflation rate of about 6.2%, and the average on-campus student will now pay about $102,000 for a bachelor's degree at a public university.

- Debt fallout: All of this has compounded to create an increasingly unstable debt situation. Household debt at the end of 2022 jumped at its fastest pace since 2007, and the grand total is sitting at around $16.5T. Many people are struggling to keep up with the cost of living, and the many observations of this conundrum are endless.

Is it still possible? The American Dream was never about being given utopia, but the opportunity to overcome challenges that stand in the way. And while it seems like it's on hold for the time being, as prognosticators often say, a regression to the mean is inevitable. | | | |

MARKETS Bond Buyers May Get Some Relief in 2023 | | | | Often a safe haven during times of market turmoil, bonds weren't exactly able to live up to their legend in 2022. Rate hikes took a toll on the bond market while stocks suffered their fate at the hands of headwinds, leaving investors with nowhere to hide. While it's certainly not quite time for optimism, there's some rational hopefulness to be found for the bond market's prospects in 2023. The fallout - Bond rout: When interest rates rise, bond prices fall. This is because new bonds are minted with a more attractive coupon rate than their predecessors, meaning demand slips on those backdated bonds, prices fall, and yields rise. 2022 was an extreme example of this as the Fed took the Fed Funds rate from around 0.25% to 4.25%, a 1600% jump.

- Collateral damage: The result was one of the worst bond markets ever. Most US bond funds are down around 13% on the year as underlying holdings like the US 10-year treasury saw yields jump more than double this year. Bonds in the private sector have suffered too as corporate bonds are similarly down. Municipal bonds, although less battered, are down noticeably as well.

The recovery - Tightening time: The Fed has brought up interest rates at an unprecedented pace, one not seen in decades as we moved 425 basis points in just three-fourths of a year. Although they're not done, the bulk of that tightening pain has already been felt by the bond market as most presume rates will end 2023 at around 5.5% or less.

- Higher yields: Bond yields have risen tremendously in the last year, and though this may hurt bondholders, it also attracts newcomers to the market. While more buyers will eventually push yields back down a bit, it will also help to buoy bond prices over the long run.

- Inflation abates: Inflation fears were another worry that kept investors shy of bonds' lower yields. As inflation hopefully continues to abate, overall interest in bonds will likely begin to regress.

Take this related lesson on this topic and earn Dibs 🟡 while you're at it: | | | |

FEATURING FABRIC BY GERBER LIFE Keeping Your Family Protected | | | | New parents have enough on their plates without spending hours navigating life insurance sales meetings. With Fabric by Gerber Life's quick 60-second quiz, you can find out what kind of coverage your family needs, and apply for a policy in just 10 minutes. - $1 million in coverage for less than $1 a day

- Coverage ranging from 10-30 years and policies from $100,000–$5,000,000

- No price changes—guaranteed

- 30-day money back guarantee, and you can cancel at any time

Qualified applicants could go from "Start" to "Covered" in just 10 minutes, no health exam required. Leave the insurance part to Fabric so you can focus on, well—life. Get a quote in less than a minute. | | | |

PERSONAL FINANCE How to Protect Your Money in 2023 | | | | From nascent markets, traditional assets to the price of everyday goods, the entire world of money and investing got roiled throughout 2022. If all the chaos taught us anything, it's that almost nothing is safe forever. While it's impossible to protect our money from everything, there are still many steps we can take to provide some safety from the threats that be. Building your money moat - Bank shop: If we include all banks across the nation, the average savings rate being paid on any given savings account is just 0.268%. If your bank is providing such a low return on your money, that alone is a sufficient reason to look elsewhere, but there are other perks too. Shop around for banks that offer better customer services, low to no fees, overdraft protection, and any other important perks you value most. It pays to have options.

- Max out: If you're able to do so, max out your retirement accounts. How does this protect your money? By protecting your future. The IRS raised contribution limits across most retirement accounts for 2023, and taking advantage makes a big difference. The extra $2,000 allowed for 401(k) holders could create an extra $227,000 over 30 years at 8%.

- Be involved: In a year as rough as 2022, it was easiest to just not look at it. While it's true that we shouldn't overanalyze our investing, it does pay to be involved. Take the time to keep a check on your investments, especially retirement accounts, and develop a healthy routine that allows you to govern them sustainably.

Take this related lesson on this topic and earn Dibs 🟡 while you're at it: | | | |

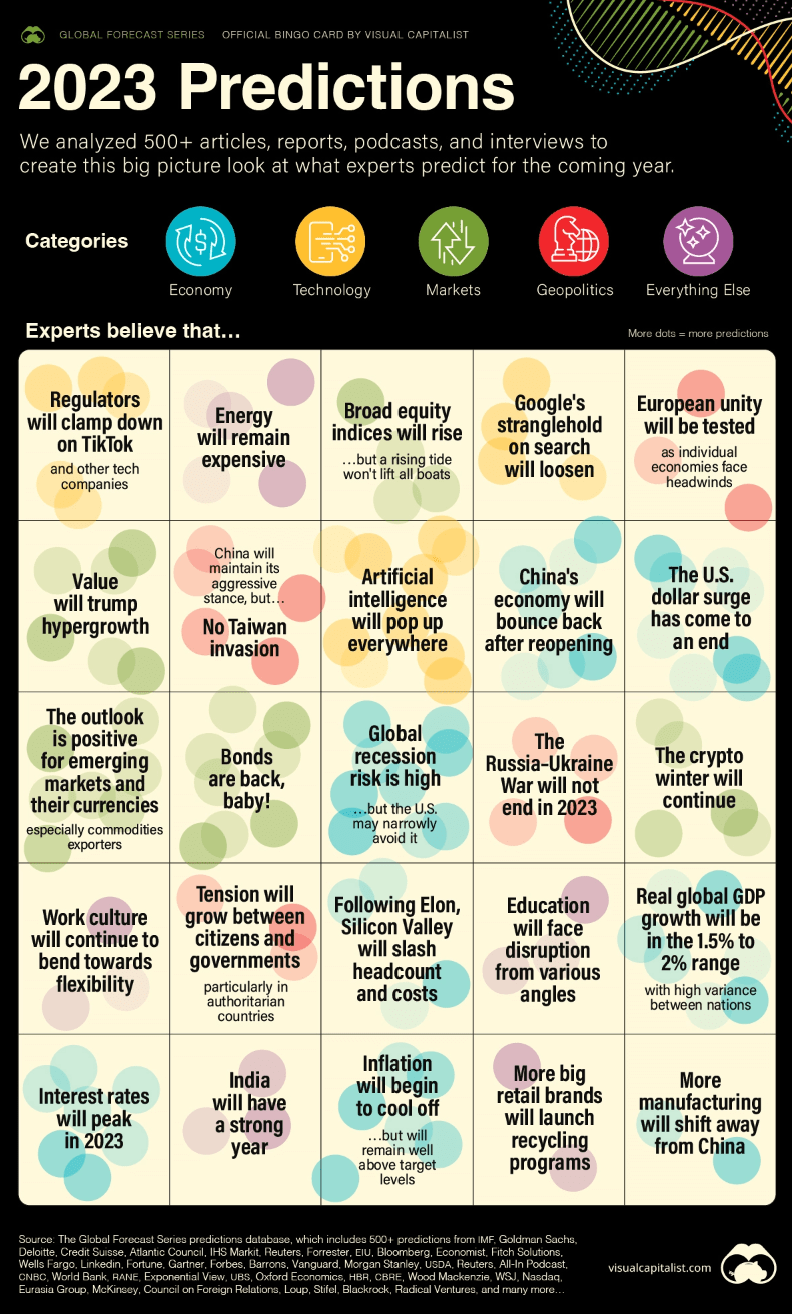

🌊 BY THE WAY | - 🔮 Answer: That "interest rates will peak in 2023" is 1 of 25 predictions for 2023, according to this Visual Capitalist analysis. Here's their map of their 25 predictions:

- 📊 Consumer prices fell 0.1% in December, in line with expectations from economists (CNBC)

- 🍳 Egg prices have more than tripled in some states over the last year - here's why (CBS News)

- 📊 ICYMI. Inflation & The Rule of 72 (Finny)

- 🌎 Why the U.S. economy needs more people (Axios)

- 📉 Finny lesson of the day. Another prediction on the above map is that global recession risk is high. Take this one if you haven't already:

| | | |

| |

| Finny is a financial wellness platform for employees. The Gist is Finny's twice-a-week (Tues & Thurs) newsletter covering personal finance, market trends and investing insights. The content team: Austin Payne, Carla Olson, Chihee Kim. Finny does not offer investment and stock advice. Please support our brand sponsor—Fabric by Gerber Life—as they make rewards on our platform possible. If you're is interested in sponsoring The Gist, please reach out to us. And if you have any feedback about this edition or anything else, please email us. | | | | | | | |

No comments:

Post a Comment